Confidence builds in Melbourne’s metro and fringe office markets: Colliers

Transaction momentum has returned to Melbourne’s metro and inner-fringe office markets, with renewed investor confidence driving a noticable uplift in activity as buyers move decisively to secure deep-value income and value-add opportunities.

Transaction volumes surge as pricing reset unlocks liquidity

According to Colliers’ latest Office Middle Markets – Australian Investment Review (Q1 2026), Melbourne’s metropolitan office market recorded approximately $476 million in transactions across 19 assets in 2025, more than doubling activity from 2024 and delivering the strongest annual result in five years.

The CBD-fringe market also rebounded positively, with investment volumes rising 17 per cent year-on-year to $189 million, as the majority of deal flow occurred in the second half of the year once buyer and vendor expectations realigned. Scott Orchard, National Director, Capital Markets & Investment Services at Colliers, said, “The uplift signals growing confidence that values have bottomed.

A pricing reset has unlocked liquidity, and buyers are now underwriting opportunities with more confidence.

Last year in metro and inner-fringe Melbourne there was a shift from opportunistic to competitive buyer behavior for well-located assets with an income bridge and that offer repositioning or refurbishment upside.”

Developers and value-add buyers re-enter the market

Developers and value-add investors were the most active buyer cohort across metropolitan Melbourne throughout 2025, accounting for close to 40 per cent of all transactions.

Much of the stock brought to market was characterised by shorter WALEs, leasing risk or vacant possession, conditions that have proven particularly attractive for buyers seeking to reposition assets early in the next cycle.

Ben Baines, Director | Investment Services at Colliers, commented, “Melbourne is following a similar trajectory to Sydney twelve months ago, with developers and value-add investors are stepping in early, targeting assets they can actively improve.

“The pricing dislocation over the past two years has created compelling entry points, particularly outside the core CBD,” he added.

Recent deals highlight renewed confidence

A series of transactions over the past year underscore the resurgence of confidence across Melbourne’s metro and CBD fringe markets (continues below).

In September 2025, 417 St Kilda Road (pictured, top) transacted for $86 million, highlighting sustained appetite for large, institutional-grade fringe assets.

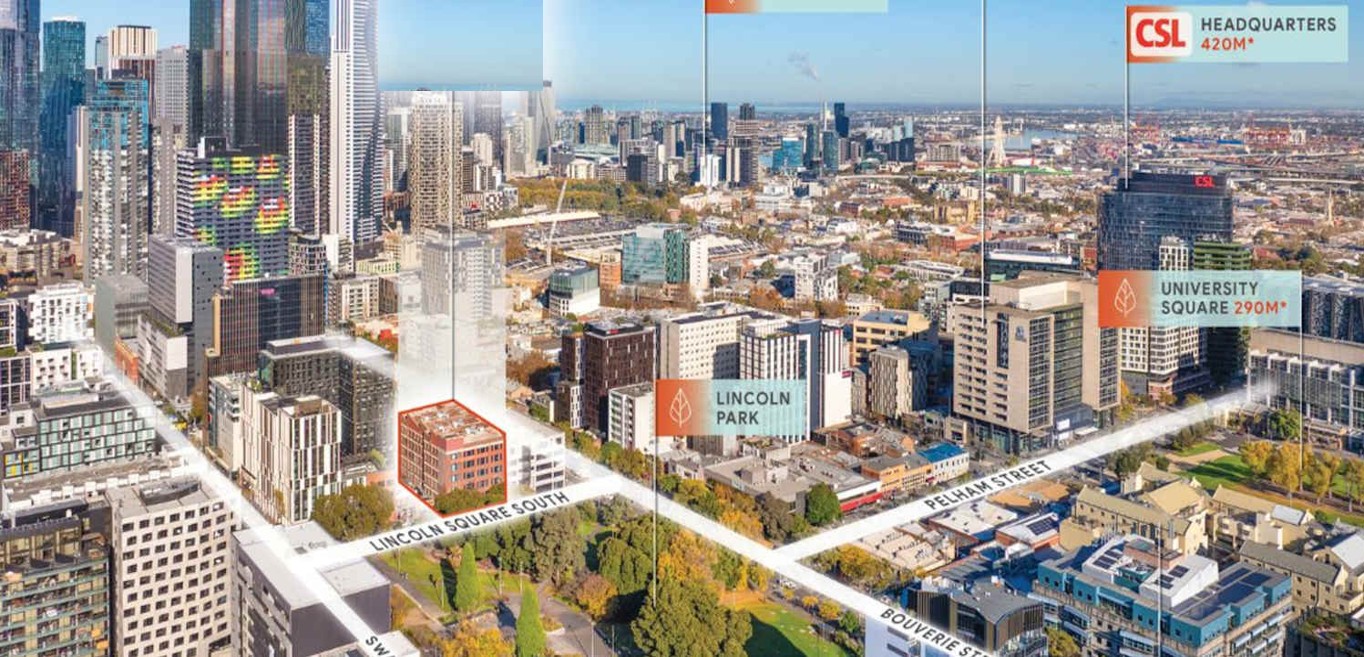

Owner-occupiers have also been active, with the sale of 23–31 Lincoln Square South, Carlton (pictured, top, right) for $19.7 million reflecting groups taking advantage of vacant possession conditions.

Metropolitan activity remained equally robust, with 91–99 Railway Road in Blackburn selling for $54.35 million late last year and Mai Capital acquiring 347–351 Burwood Highway in Forest Hill for $36.6 million, demonstrating deep demand across middle-ring suburban markets.

Local capital drives inner-fringe recovery

Domestic private capital played a leading role in the CBD fringe recovery during 2025, with high-net-worth investors and family offices accounting for more than half of total transaction volumes.

These buyers have increasingly targeted counter-cyclical opportunities, accepting softer near-term income in exchange for long-term upside as vacancy stabilises and the forecast new supply pipeline diminishes.

“Local capital understands these precincts intimately,” Mr Orchard said. “Buyers are backing locations with strong long-term fundamentals, in activity centres on top of public transport, near retail, wellness and lifestyle infrastructure, and they’re prepared to look through current uncertainty and take a medium to long term view as markets normalise.”

Outlook: steady activity expected through the remainder of 2026

Looking ahead, Colliers expects transaction conditions across Melbourne’s metro and inner-fringe office markets to remain constructive through the remainder of 2026.

Buyer depth remains improved on previous years, new supply is limited, and investors are increasingly differentiating between high-quality assets and secondary stock.

While interest rates are expected to remain higher for longer, much of this risk is now reflected in pricing, with competitive tension returning for assets that can be repositioned efficiently or deliver secure income.

A link to the report is here.