Metropolitan office markets outlook, 1H2021: Colliers

Twelve months ago, the Australian office workforce was very much settled into the work-from-home routine and many questions were being asked of not just how businesses will re-occupy offices, but where will we occupy office space moving forward.

We all clearly remember the chimes of decentralisation and hub-and-spoke strategies.

However, with leasing activity starting to gather pace through the start of 2021, are we starting to see these strategies come to fruition?

The answer at present, is no.

Leases signed over the first three months of 2021 would have been planned and negotiated with the impacts of COVID on office occupancy most certainly a consideration.

Hence, current deal activity should start to give us an idea of any significant locational shifts starting to emerge.

A total of 162 deals have been signed for across all of Australia’s major office markets and negotiated by Colliers over Q1 2021.

Of these, 84 were signed within the CBD and 78 across the non-CBD markets.

However, only 11 deals across 5,200 sqm are attributed to occupiers decentralising from a CBD to a non-CBD location.

This was offset by 12 deals across 4,250 sqm of centralisation activity to our CBD’s, so the opposite trend does not hold true either.

And what of the previous notion that a hub-and-spoke would be adopted by companies with the spoke being a suburban location?

Once again, we have not seen any evidence of this being adopted to date.

Over the last six months it has become apparent that a lasting trend from COVID is that the spoke is work-from-home or a flex-space arrangement and the hub is either a CBD or non-CBD location dependent on the needs of each specific business.

Flex-space within suburban locations is still very much being discussed by operators who are searching for suitable space to operate and by businesses that are contemplating whether they can offer flex-space options closer to home for their employees.

However, these are decisions that cannot be made rapidly and will take time to play out. We expect to have a clearer picture of potential suburban flex space trends by the end of 2021 and into 2022.

So what relocation activity is occurring?

When we breakdown the deal activity to reveal where occupiers are moving from, 72% have ‘moved within’ – that is moved within the CBD or moved within or between a non-CBD office precinct.

Decisions surrounding an occupier’s location are not taken lightly and excluding cost factors, many variables are taken into consideration such as; workforce demographics, requirements for connectivity to client and stakeholder locations, company culture and brand and the desired location for a company’s longer term strategy and growth projections.

Instead of pivoting on previous strategies which have fulfilled these requirements, tenants are still relocating with their previously chosen strategy in mind.

To make a U-turn on these plans with no significant change in their strategy would be a costly exercise and one that will not be easy to unravel overnight.

There is some evidence emerging of relocation between non-CBD locations within the same catchment area which is being spurred by a flight to quality and amenity.

This has been enabled by a wave of new supply across Australia’s non-CBD markets with 257,100 sqm of newly developed or refurbished stock entering the market over 2020.

This is the largest amount of new supply added to the non-CBD markets since 2009 and equates to 3.5% of total stock.

Markets such as North Sydney and Richmond/Cremorne in Melbourne and Fortitude Valley in Brisbane are examples of major beneficiaries of occupiers leasing space in newly developed buildings relocating from metro locations such as Macquarie Park and Norwest in Sydney,the Outer Eastern suburbs of Melbourne, and Brisbane Fringe precincts.

This has been evident with 1 Denison, North Sydney, which has seen tenants such as Nine Entertainment Co. relocate from the alternate suburban locations of Willoughby and Frenchs Forest, and Microsoft and Luxottica relocate from Macquarie Park, in addition to Datacom from North Ryde.

Another positive sign for the non-CBD markets is that deal activity over the first quarter has been robust from sub-1,000 sqm occupiers. 54% of deals within the CBD were across smaller tenancies and 67% of non-CBD deal activity was recorded in the sub-1,000 sqm category.

Whilst the higher percentage of sub-1,000 sqm deals is not surprising for non-CBD locations given the higher percentage of SME occupation, it is a positive sign that these occupiers are still invested in leasing office space given their more agile nature and ability to uproot more easily to a work-from-home model.

If anything, the need for collaboration to drive innovation and increase productivity is paramount now more than ever for SME’s who have a growth strategy front of mind.

However, there does appear to be some uncertainty. Major corporates and larger occupiers generally take longer to make significant real estate decisions and may still look to scale back their office footprint by some degree, affecting non-CBD office locations.

Locational strategies continue to be occupier specific with CBD, Fringe, Metro, work-from-home, and flex-space all options that can be interweaved to create the right real estate strategy for each business – there is no one size fits all. The pandemic has heightened the demand for alternative choices of where to live, work and play and the interconnection of these components of life.

Australia’s non-CBD office markets are in a unique position to capitalise on this demand as continued infrastructure and regeneration projects occur and new next generation office buildings leverage on these transformations to create an ‘experience’ and not just a place to work.

Sydney

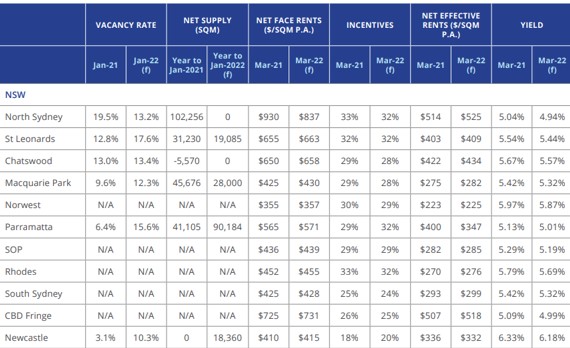

Average A-grade face rents are continuing to hold steady increasing by just 0.4% over the last six months (to March-21) across the majority of the Sydney Metro office markets, despite downward pressure from rising vacancy.

Chatswood recorded the strongest positive growth of 4.0%.

However, this is due to the market witnessing less frequent lease transaction activity due to the smaller nature of office stock, and therefore recent deals reflect a broader increase to rents inline with other markets.

A disparity between A and B grade assets is starting to occur as a flight to quality across our major office markets emerge. Average B-grade net face rents have declined by -1.0% over the last six months, driven by decreases within Parramatta (-3.0%), CBD Fringe (-1.8%) and St Leonards (-1.6%).

We are expecting further downward pressure on secondary face rents over the next 12 months alongside rising incentives as smaller tenancies may look to upgrade to higher quality existing stock or flex-space operations.

Leasing activity is starting to gain momentum and there is confidence that activity will gather pace through 2021 with positive signs in the recovery of labour Markets across Sydney.

Colliers office leasing signed 20 deals totalling 6,655 sqm across Sydney’s Metro markets over the first three months of 2021.

This is a decrease from the same period last year, but a healthy sign that occupiers are starting to action leasing decisions after 12 months of reluctance.

Investment markets have remained healthy over the last 12 months despite pressures on occupancy. Although only five assets totalling $315.2 million have transacted across Sydney’s Metro office markets over Q1 2021, we anticipate further activity over the remainder of the year as investors look for opportunity across the Sydney markets as a preferred location.

Melbourne

Melbourne Metro enquiry has gathered pace from the end of 2020 and continuing through to the beginning of 2021 as occupiers gain confidence to make leasing commitments.

Colliers signed 30 deals across 22,500 sqm over the first quarter of 2021.

The number of deals signed over Q1 2021 is 50% higher compared to the same period in 2020.

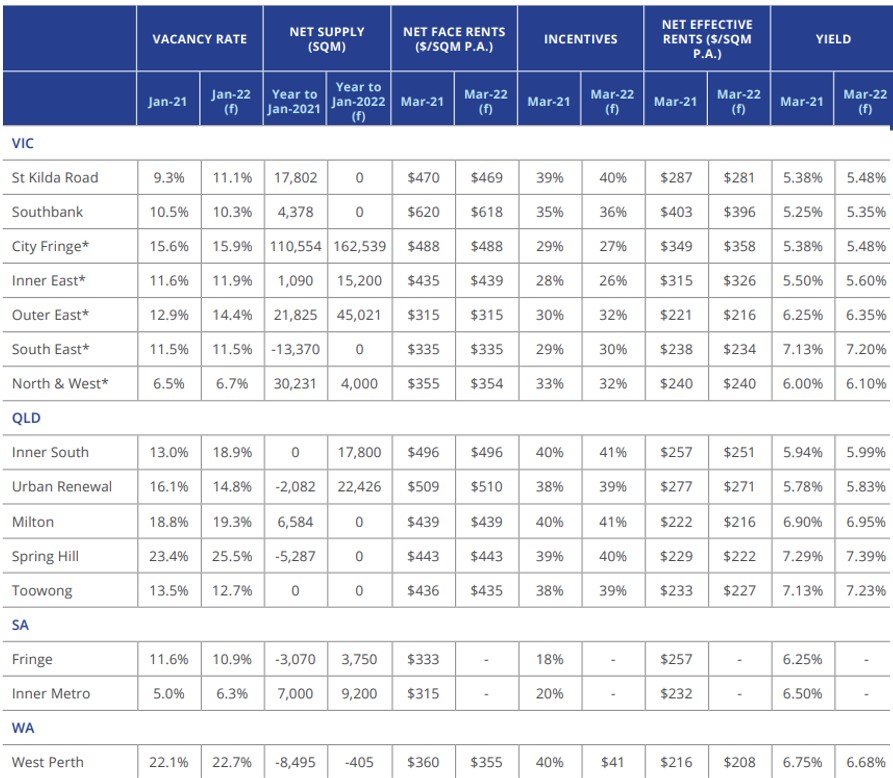

We expect a flight to quality and strong interest to Melbourne Fringe office locations to generate healthy activity levels over the remainder of the year.

Average A-grade face rents across the Metro markets have increased by 1.8% over the first three months of 2021.

This is partly a function of a hiatus in deal activity last year and low confidence translating into lower rental levels from late 2020.

However, as deal activity reignites, which we have seen through 2021, face rents being achieved are closer to and in some cases above what was recorded pre-pandemic.

However, downward pressure will remain on secondary assets as the flight to quality takes shape.

Healthy levels of capital are still looking to be placed across Melbourne’s metro office markets, however, transactions over the last 12 months were limited. Over Q1 2021 five assets totalling $49.3 million has transacted mainly within the City Fringe and Inner East precincts and South Eastern corridor.

As confidence continues to gain momentum in Melbourne’s office markets, we expect further activity to come to fruition over the remainder of the year.

Brisbane

A recent uptick of Urban Renewal take-up across high quality A and B grade buildings demonstrates that the recovery of the leasing market has well and truly started, at least within some precincts.

The increasing availability of high-quality stock has allowed occupiers to relocate and upgrade office accommodation in many instances at neutral costs.

This trend is expected to continue at least over the remainder of 2021.

Gross face rents continue to hold steady since March 2020.

Incentives have become a decisive tool during the negotiation process underpinning an increase in A and B grade average incentives to 38%-39% by March 2021.

As a result, average net effective rents have contracted up to 6% over the past year. Circa 43,000 sqm of new development supply with a pre-commitment rate of 32% is expected to reach practical completion in 2021.

The Urban Renewal precinct is expected to see the completion of two projects (Mater building in Newstead and Jubilee Place) and expand by 25,250 sqm with a 62% pre-commitment rate at the time of writing.

The Inner South precinct is expected to see an increase of speculative office stock of circa 17,800 sqm following the completion of the Mobo project in September 2021.

The increase of Prime grade stock is expected to put upward pressure on metro vacancy potentially to range of 17%-17.5% by late 2021 (story continues below).

The investment market (above A$5 million) has continued its gradual recovery over the first quarter of the year. Preliminary data for Q1 2021 reveals a total of circa A$109 million of Brisbane metropolitan office buildings transacted. However, investment volumes are expected to remain below the 2017-2019 investment boom period and below the long-term average over the next twelve months

Adelaide

Vacancy in both the Adelaide Fringe and Metro office markets has fallen in the second half of 2020.

Adelaide Metro markets saw vacancy fall to 3.5% from 5.3%, with Adelaide Fringe falling to 11.6% down from 14.4%.

Colliers Demand Index has shown an increase in enquiry in metro markets at the beginning of 2021 with enquiry remaining stable for the Fringe market from 2021 compared to 2020.

The majority of this enquiry is for space below 500 sqm.

Sales volumes in the Adelaide Metro & Fringe markets totalled $177.3 million in the year to March 2021.

This was boosted by the sale of the yet to be constructed SA Emergency Services Command Centre for $103 million.

This was sold by Axiom and purchased by Charter Hall, with a quoted yield of 4.8%. Bridgestone has moved into their new premises at 210 Greenhill Road, Eastwood which was completed in the first quarter of 2020.

Other major projects currently under construction include the redevelopment of the Cancer Council site at 202 Greenhill Road, Eastwood; Raytheon’s new facility at 1-11 Technology Drive, Mawson Lakes; and Mitsubishi’s new HQ at James Schofield Drive, Adelaide Airport

Perth

The rise in Perth CBD vacancy to 20% has generated additional competitive pressures for the Perth metropolitan office market, where vacancy has remained generally stable at levels of between 16% to 22.1% (in buildings over 1,000 sqm) for the major office precincts over the past six months.

As a result of the increasingly competitive environment, and more recently with the work-from-home trend, landlords are reassessing their expectations and have been sharpening offers to fill vacancies or maintain occupancy levels.

In West Perth, over the past six months average A grade rents have reduced two percent and incentives have increased 2.5 percentage points to average 40%.

Despite the rising CBD vacancy, the West Perth market was stable over the six months to January 2021.

Vacancy continues to be dominated by B-grade stock where 48,611 sqm was reported vacant by the Property Council of Australia in January 2021.

A-grade vacancy was 21,629 sqm or 23.9%.

Vacancy is expected to remain generally stable in West Perth and other suburban office precincts over the next twelve months. However, resource sector investment activity is improving and West Perth, being the traditional favoured location for small to medium mining and energy companies, may see some upside in net absorption if project space demand increases bringing forth a quicker improvement in vacancy

Newcastle

The Newcastle A Grade market has seen a slight increase in vacancy, with PCA statistics showing an increase from 1.4% to 3.1% over the 12 months to January 2021.

ASX listed insurance company nib subsequently put 3,159 sqm on the market for sub-lease, increasing the overall A Grade vacancy to 6.3%.

The B Grade market however has improved with vacancy reducing from 7.8% to 5.9%, aided by budget conscious tenants relocating from A grade to B grade buildings.

Whilst A grade office vacancy is anticipated to increase over the next 12 months, we are also likely to benefit from a maturing market.

Leasing enquiry has increased following the pandemic as national businesses and government look at decentralisation, with well-located and connected regional cities their focus as they aim to reduce business interruption.

Demand has been coming from co-working operators, with Wotso committing to a 1,000 sqm B grade building in the emerging Newcastle West precinct.

Investment demand has continued, although not unlike all markets their has been a lack of quality investment options available to satisfy the weight of capital available.

One commercial asset transacted above $10 million throughout 2020 across the Central Coast and Hunter Regions, compared to nine sales in 2019.

Given the changing leasing dynamics, we witnessed two office buildings commence construction in 2020 which will add approx. 21,500 sqm of A grade accommodation to the market in 2022.

One of the buildings relates to a fund-through of a 16 storey commercial building by HWG, which represents the largest office transaction on record in the Newcastle market.

Gold Coast

Commercial leasing activity is rebounding through the recovery stage, with vacancy expected to fall below 14% gradually approaching the 20-year average of 13.4%.

Over the first quarter of 2021 we have seen a large take-up of A grade office space of 5,000 sqm within the Robina-Varsity Lakes precinct from a telecommunications company expanding operations and relocating from Broadbeach.

This deal is an early indication that some businesses within the region are in expansion mode.

In response to the increase in vacancy and uncertain outlook of the office market during 2020, average A and B grade incentives increased in the range of 2.0 pps – 3.6 pps, putting downward pressure on net effective rents in the range of 3.0% to 7.0%.

Over the first quarter of 2021, market conditions have definitely improved so we have seen some gross face rental increases in the precincts of Bundall B grade and Southport A grade while incentives have generally stabilised at 2020 levels.

We expect to see rental stability dominating the leasing market in 2021. The renewal process of the office market is well and truly under way, and it is expected to peak over the next 12-24 months.

A pipeline of circa 13,600 sqm of fully pre-committed new developments within the Robina-Varsity Lakes precinct are currently under construction or approaching construction stage.

This includes the Alceon development pre-committed to TAFE and the QIC development pre-committed to Services Australia. Investment sentiment is improving regionally, albeit investment activity remains concentrated on sub-A$5 million transactions.

In the case of A$5+ million assets, sales evidence was very limited in 2020 (5 sales for a total of A$37.9 million) and this trend is expected to continue this year as landlords are not willing to make divestment decisions in the absence of alternative competitive investment opportunities.

By Joanne Henderson, national director, Research

Capital Markets Outlook

The metro office investment market bounced back in the last quarter of 2020 which is a sign of improved sentiment in office markets more generally.

Total investment volumes for the year to March 2021 totalled $4.242 billion which was 48% lower than in the prior 12 months.

The first quarter of 2021 was softer seeing $457.9 million of sales which was 63% lower than in Q1 2020.

Metro market sales accounted for 43.8% of the total office transactions in the year to March 2021 compared to 38% in year to March 2020.

Investors were more confident in metro markets with several investors expecting that demand in metro office markets would be stronger in the short term. Sales volumes were substantially impacted during the second and third quarters with deal flow being interrupted due to people movement restrictions.

The Melbourne metro office market saw the largest decline in sales with only $540.64 million sales in the year to March 2021 which was 67.7% lower than the prior year.

This was reflective of the longer social distancing restrictions in place to suppress the outbreak on Melbourne between July and October 2020. Perth Metro sales volumes were down 55% in the year to March 2021 with Sydney Metro down 49.4% and Brisbane Metro down 25.5%.

The Adelaide and Canberra Metro markets were the only markets to see higher sales volumes and were up 117.8% and 32.7% respectively. Institutional investors still dominate sales volumes accounting for 59% of all sales in the year to March 2021.

This was however lower than the share in the prior year which was 63% which is in line with the five-year average.

Private investors accounted for a slightly larger proportion of the sales volumes in the year to March 2021.

Capital was mostly sourced from Australian investors accounting for 59.3% of the total sales volume.

Offshore investors accounted for 35% of total sales volumes with the remaining transactions source of capital being undisclosed.

Over 80% of the offshore capital is sourced from the Asia region with most of the capital (71%) being sourced from Singapore.

Metro markets have remained an attractive investment for investors with employment within metro locations recovering faster than in CBDs and in some cases being above pre pandemic levels.

Metro markets which offer great amenity and are part of a transport hub continue to remain in demand and are a good alternative to CBD markets with lower asset values making metro markets an affordable and attractive investment.

With a robust weight of capital still evident in the market, we expect investors to continue to look aggressively across both metro and CBD office locations for investment opportunity.

By Kate Gray, director, Research

This is an excerpt of Colliers’ Metro Office 1H2021 analysis, edited and published with permission.

The report can be accessed following this link.